#1 AI stock trading for $3

Sponsored

AI is by far the biggest tech investing trend of 2023. But Ross Givens says the #1 artificial intelligence stock is NOT Microsoft, Google, Amazon or Apple. Nope – his research is pointing to a tiny, under-the-radar stock that's trading for just $3 right now… And could soon shoot to the moon, handing early investors a windfall. This company already has 98 registered patents for cutting-edge voice and sound recognition technology… And has lined up major partnerships with Honda, Netflix, Pandora, Mercedes Benz and many, many others. So if you missed out on Microsoft when it first went public back in 1986… This could be your shot at redemption. Click here now for the full details of this $3 stock that's set to rocket in the AI revolution…

At a time when the S&P 500 index is yielding just 1.5%, finding a stock with a yield of 12.8% might seem like finding a needle in a haystack. That lofty yield is exactly what Annaly Capital Management (NLY 1.16%) is offering investors today. But it is not a needle in a haystack or a diamond in the rough. If history is any guide, it could very well turn out to be a yield trap.

Here are three facts you need to know if you are considering buying Annaly today.

1. Annaly is not your typical REIT

As a real estate investment trust (REIT), Annaly is required to pass at least 90% of its income on to shareholders. That said, it does not do what most REITs do. A traditional REIT owns physical property and leases it out to tenants. That's a fairly simple business model designed to generate a consistent income stream. Instead, Annaly invests in mortgages.

Technically, mortgage REITs like Annaly usually buy bond-like securities that represent a pooled collection of mortgages, often called something like a collateralized mortgage obligation (CMO). CMOs do generate cash flows based on the payments on the underlying mortgages. However, there's a lot more going on than in a traditional lessee/lessor relationship. For example, CMOs trade openly so their value can change day to day, the price of a CMO will vary along with interest rates, and payment trends and housing market dynamics will also play a role in prices.

Then there's the fact that mortgage REITs like Annaly tend to use leverage to enhance returns. The portfolio of mortgages is often used as collateral for that leverage, which can be a problem if CMO values fall dramatically. But the end goal is to make more from the interest collected on the mortgage portfolio than it has to pay in interest on the leverage it has taken on. That's a spread trade, and it's very different from owning a physical property.

All told, if you want to buy Annaly, you'll need to take extra time to make sure you fully understand the business you are buying. It may not be what you think it is if you are used to buying property-owning REITs.

2. Annaly's yield isn't as great as it looks

There's risk with any stock investment, of course. And a high yield can be an indication that Wall Street isn't confident about a company's ability to pay its dividend. That's exactly how investors should view Annaly's huge 12.8% dividend yield. The proof is in the numbers.

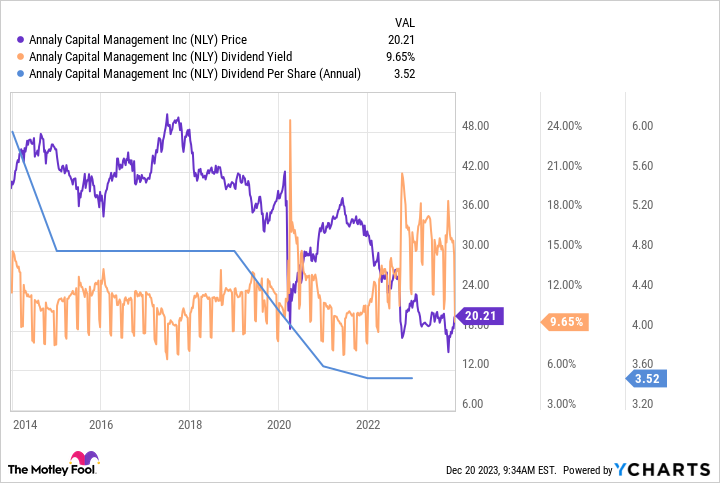

The chart above is a bit busy, but it paints a very worrisome picture. The first line to consider is the orange one, which is the dividend yield. Notice that the yield has always been fairly lofty, usually above 10%. Yield is a simple math equation, taking the annualized dividend and dividing it by the share price. This is where the trouble begins.

The blue line represents Annaly's annual dividend. Notice that it has been trending lower for a decade. Given the equation above, the only way the yield can stay high under this scenario is if the stock price also declines, which is exactly what the purple line shows took place. If you are a dividend investor trying to live off of the income your portfolio generates, buying Annaly a decade ago would have left you with less income and less capital today. That's most certainly not the outcome you would have hoped for.

3. Annaly isn't really meant for small investors

By this point, most income-focused investors will probably understand why a mortgage REIT like Annaly isn't going to be a good buy candidate. But that doesn't mean that Annaly won't be appropriate for some investors. The key is that Annaly is a total return investment, which assumes the reinvestment of dividends.

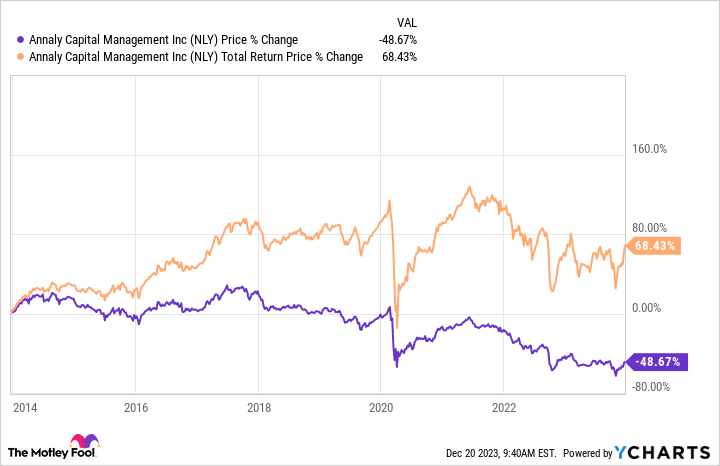

As the chart above highlights, the stock price return was negative over the past decade. But if dividends were reinvested, the total return was positive. Annaly's function is to provide direct exposure to mortgages for investors that focus on asset allocation. That generally means large investors like pension funds and insurance companies that think in terms of total return, and not small investors looking to generate a reliable stream of dividend income.

Annaly is probably not going to be for you

At the end of the day, Annaly has a huge yield that will probably seem attractive until you dig into the backstory here. It is a complicated investment that serves a niche purpose that simply won't be appropriate for most investors. Tread carefully if you are thinking about buying Annaly because for years it has been little more than a yield trap for individual investors.

Like Buying Microsoft in 1986… at Only $3?

Sponsored

Most investors aren't seeing it, but… There's a new bull market that's quietly raging. Have you ever opened your cell phone with Face ID? Paid for something using your credit card? Jumped in your car and plugged your destination into Google Maps? If so, you've benefited from this “secret megamind” technology… And Ross Givens has just identified his #1 stock pick to ride this revolutionary tech to a potential windfall gain… The likes of which haven't been seen since Microsoft went public in '86. Right now the stock trades for just $3… But according to Ross' research, it could soon explode to obscene levels… And give your retirement a much-needed “booster shot.” You better move quick – click here for the full details right now…