WARNING: Mandatory U.S. Dollar Recall to Begin on January 31st?

Sponsored

If you have any U.S. dollars in your bank account… You must see this shocking video exposing the government's new plan to recall the U.S. dollar. According to Business Insider, this recall “could be imminent.” And if you don't prepare now, you could end up holding a bunch of worthless U.S. dollars. Click here to see the three simple steps you can take now to protect your life savings.

I've been accumulating shares of Brookfield Renewable (BEPC 3.17%) (BEP 2.85%) for several years, and the renewable energy juggernaut has grown into one of my largest positions. Because of that and its high-yielding dividend, it's one of the top income producers in my portfolio.

Despite having an already meaningful allocation, I plan to continue adding to my position next year. Here's why I can't stop buying this top-notch income stock.

A sustainable payout

The main draw of Brookfield Renewable is its dividend, and it has the three things I seek in a dividend stock:

- An above-average yield: Its yield of 4.7% at the current share price is a lot higher than most stocks. For comparison, the dividend yield on the S&P 500 is around 1.5%.

- Sustainability: Brookfield produces lots of recurring cash flow, has a reasonable dividend payout ratio, and has a strong balance sheet.

- Dividend growth: The company has increased its payout by at least 5% annually for the past dozen years.

I've learned the hard way over the years that a high-yielding dividend is only worth it if the underlying business can sustain that payout. Brookfield has gone to great lengths to ensure the sustainability of its dividend. It all starts with the company's cash flow. Brookfield sells the bulk of the electricity it produces under long-term, fixed-rate power purchase agreements (PPAs), with 90% of its power under contract for an average of 13 years. About 70% of those contracts link rates to inflation. Those inflation-linked PPAs alone will add 2% to 3% to its funds from operations (FFO) per share each year.

Brookfield also has a diversified portfolio by technology (hydro, wind, utility-scale solar, distributed generation, and energy storage), geography (North and South America, Europe, and the Asia-Pacific region), and customers (utilities and corporate buyers). That diversification helps reduce its risks while enhancing its growth prospects.

Finally, Brookfield has a fortress-like balance sheet. The company has a good bond rating (BBB+), virtually all of its debt (98%) is fixed rate, with no material near-term debt maturities, and it has significant liquidity ($4.4 billion at the end of the third quarter). That gives it the financial flexibility to invest in development projects and make value-enhancing acquisitions. Brookfield also routinely recycles capital by selling mature assets to fund higher-return new investments. The company has raised $600 million from asset sales over the past 18 months to fund new investments.

High-powered growth and total returns

Brookfield Renewable's high-yielding dividend is only part of its appeal. The company has an excellent track record of growing shareholder value by increasing its earnings and dividend payments. Over the last decade, Brookfield has grown its FFO per share at a more than 10% annual rate. That has given it the power to increase its dividend payments at a 6% compound annual rate. This combination of growth and income has resulted in a 13.7% average annualized total return over the past decade (beating the S&P 500's 12.3% average annualized total return).

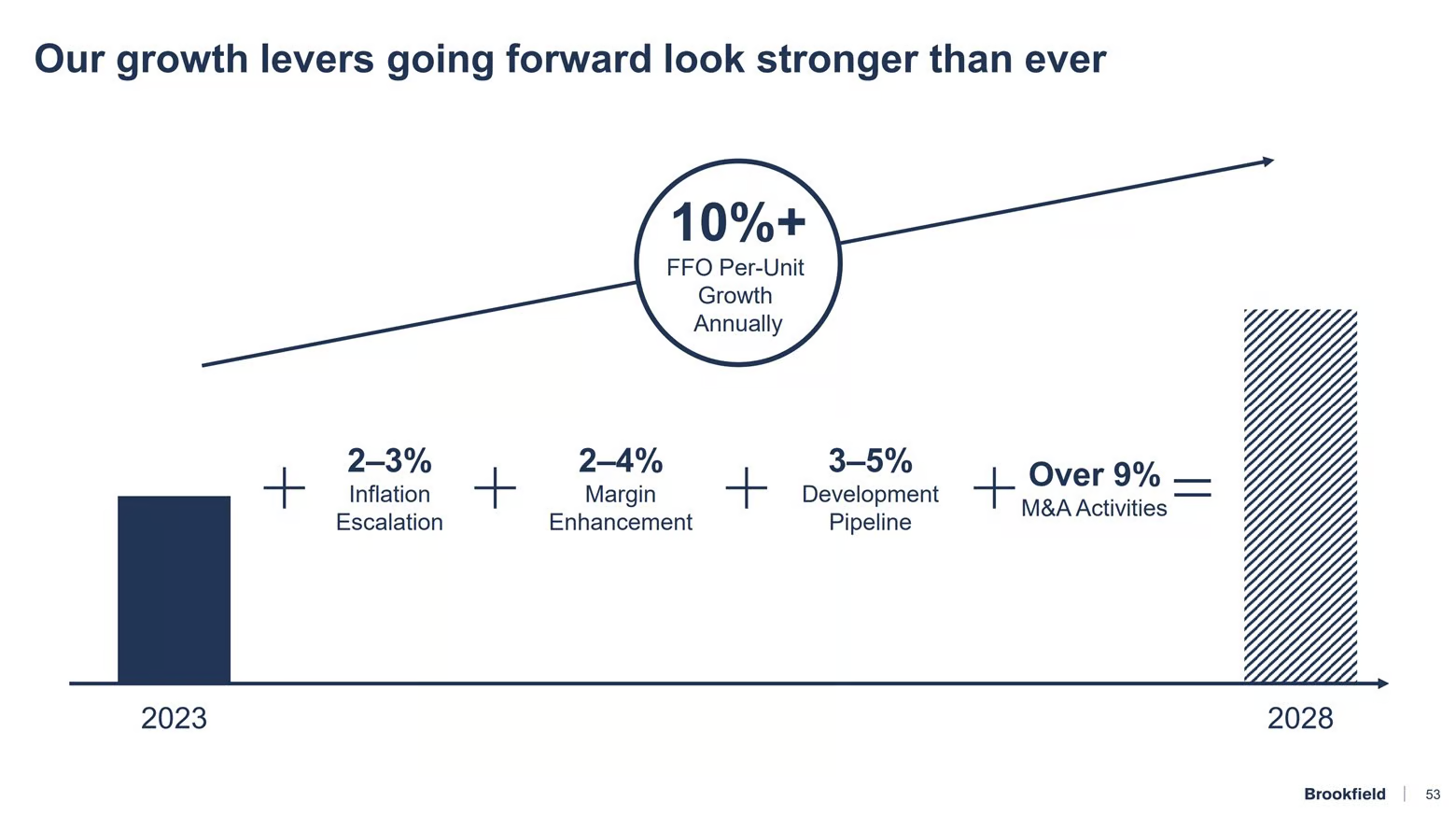

The company is in an excellent position to continue growing shareholder value. Brookfield has a quartet of growth drivers that should power 10%-plus FFO-per-share growth through at least 2028.

Brookfield's inflation-linked contracts provide a nice base growth rate. Meanwhile, margin enhancement activities, such as locking in higher power rates as legacy contracts expire, will further increase the cash flows of its existing portfolio assets. On top of that, Brookfield has an extensive pipeline of renewable energy projects under development that will grow its cash flows further. Finally, acquisitions can provide a meaningful boost to its bottom line. It has closed three deals over the past few months (with more in the pipeline), which should give it the power to deliver 10%-plus FFO-per-share growth in 2023 and 2024.

The company's growing cash flow should enable it to continue increasing its high-yielding dividend. Brookfield's long-term target is to increase its payout by 5% to 9% annually. Add that high-yielding and steadily rising payout to the company's growing earnings, and it should have the fuel to continue producing double-digit percentage total annual returns.

The complete package

Brookfield Renewable checks all the boxes for me. It pays a sustainable, high-yielding dividend that should continue rising at a decent clip as the company's earnings grow. With a nearly 5% yield and 10%-plus earnings growth, it should have the power to produce double-digit total annualized returns. That combination of low risk and the probability of earning a high return is why I continue buying shares of this renewable energy giant.

AI “wealth window” will close January 9, 2024?

Sponsored

Hello. I'm James Altucher. I've been called a “genius investor” by my fans… And an “eccentric millionaire” by some others. I think it's because I make big predictions… That tend to come true. Today, I'm making my boldest prediction ever. Next-generation AI technology will create the first $100 TRILLION industry. And there could be trillions available to those investors who get in early. I put together this personal video [HERE]… Revealing the AI stocks I believe… Could turn as little as $10,000… Into $1 MILLION over the next few years. If you get in early, this one-time opportunity could… Potentially change your financial circumstances… For you, your family, and your heirs. Today, I want to show you how I believe… AI 2.0 will open a brief “wealth window”… That will slam shut January 9, 2024. If you've missed out on new tech opportunities before…. I urge you, do not ignore this message. HERE is everything you need now.

P.S. To show you I'm serious about helping you get in on this opportunity, I'm giving away one of my top 5 AI 2.0 stock picks – free. See my top 5 pick here now.