Hidden Payouts in Congress Bill (Claim Your Share)

Sponsored

Congress just opened up a new income stream that very few Americans are aware of. See, buried among the fine print in the recent Inflation Reduction Act… Is a directive that's channeling billions of dollars to “special” EV service firms. And the best part is these firms are required to share a large chunk of their profits with ordinary Americans. In fact, I estimate there's $563 million up for grabs this year alone. The first payment is scheduled for January 17th. So you'll need to move fast on this one. Click here to discover this incredible new EV opportunity while it's available.

P.S. This could net you up to $34,200 per year in easy, passive income. It takes just five minutes to set up, and after that you won't need to do another thing. But you'll need to take action straight away.

by Jody Chudley

Investing is a cyclical business.

The performance of emerging markets this century is proof of that.

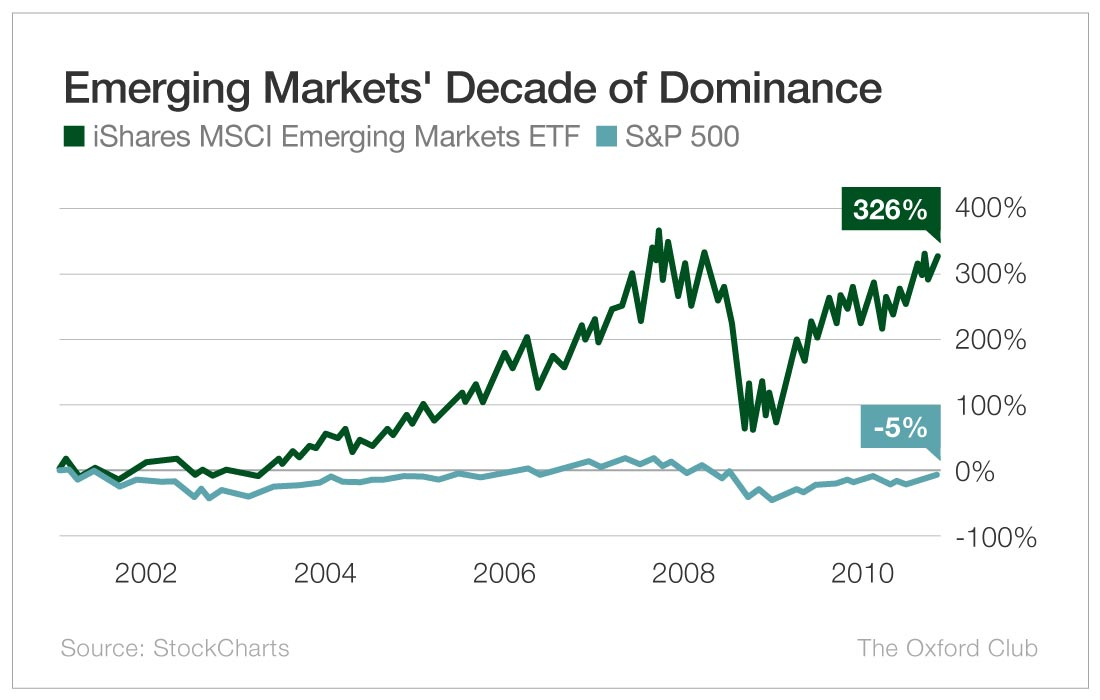

From 2001 to 2010, emerging markets were the darlings of the investment world. Everyone loved the high-growth opportunities in emerging economies.

Over that decade, it paid well to have exposure to emerging market stocks. They massively outperformed the S&P 500.

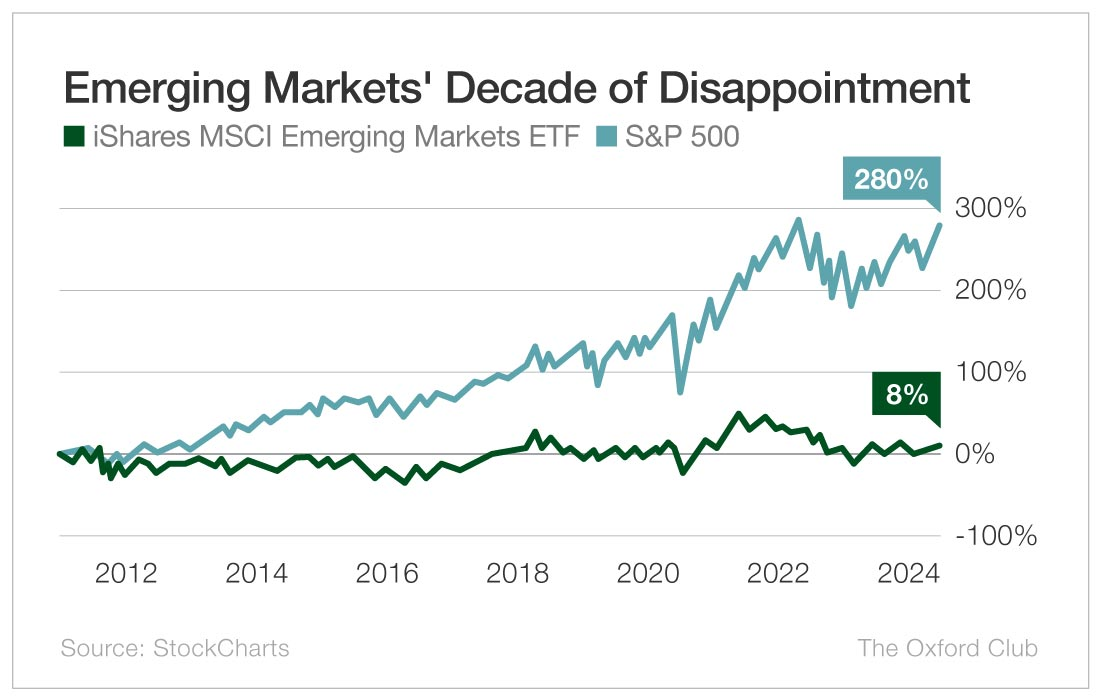

Since then, the cycle has turned, and it has turned hard.

Emerging markets have performed terribly, and they’ve been a huge drag on portfolios.

Not only have they badly trailed the S&P 500… they’ve gone absolutely nowhere.

There is, of course, a reason for these cycles.

At the start of the century, the S&P 500 was extremely expensive and emerging markets were cheap.

What followed was a decade of emerging market outperformance.

Owning emerging market stocks over that time frame was profitable because they were attractively priced going into it.

After that decade of outperformance, emerging market stocks became expensive and S&P 500 stocks became attractively priced.

That was what set up this past period of underperformance in emerging markets.

But it’s time for the cycle to turn again.

There is terrific value here, and now – at the start of the next phase of the cycle – is when you want to be buying.

Sendas Distribuidora (NYSE: ASAI) is a fast-growing company that is available at a very attractive price and is based in an emerging market.

Sendas operates a discount grocery store chain in Brazil under the Assai brand.

I like to think of Sendas as the Costco of Brazil.

While the company doesn’t charge a membership fee as Costco does, it offers discounts on bulk orders of food and household items and sells them in no-frills, warehouse-type stores.

Sendas is also similar to Costco in that the value it offers to customers is a competition killer and its business model is all about sustainable long-term growth.

To fast-track that growth, Sendas acquires less appealing competitor stores in prime locations and then converts them to the much more successful Assai brand.

From 2011 to 2023, Sendas grew its store count to 288 locations and increased its revenue at an incredible annualized clip of 26%.

And the company still has a huge growth runway in front of it.

Of the 203 cities in Brazil that have populations of more than 150,000, 91 still don’t have a single Assai location.

Furthermore, on a per-capita basis, Brazil still lags the developed world in food spending.

As more and more of Brazil’s population moves into a middle-income lifestyle, consumers will spend more and more money at Assai stores.

That is a tailwind that will last for a long time.

If emerging markets were in favor with investors, I would expect this high-growth company to be selling at a rich valuation.

But with emerging markets in the doldrums, we can buy shares of Sendas today at a very, very appealing level.

At their current trading price, Sendas shares are offering a 25% free cash flow yield based on the company’s expected 2025 financial performance.

Here’s another way to look at it: The stock is currently trading at less than 12 times forward earnings.

These are very inexpensive valuations for such a fast-growing company…

But please keep in mind that investing in emerging markets is riskier than investing in developed markets.

That means you should take much smaller position sizes so you can keep most of your portfolio focused closer to home.

At Sendas’ current price, I would have classified it as “Extremely Undervalued” if it weren’t for the elevated risk that comes with investing in emerging market stocks.

But with that extra risk in mind, The Value Meter rates Sendas Distribuidora shares as being “Slightly Undervalued.”

A 10,000% Dividend?!?

Sponsored

Have you seen this strange oil investment? It's NOT a stock, bond, or private company… It has NO age requirements… You do NOT need to be accredited to participate… And you can get in for as little as $25. Yet this secret is so powerful that one man used it to build a $100,000 income stream from just $1,000. And he was collecting this income even 50 years later! That's like earning a 10,000% dividend year after year! In short… This is easily the #1 Oil Play for 2023 and beyond. My short presentation reveals everything: