It was just two short years ago that investors looking to pivot away from stocks and into cash needed to effectively accept zero return for the privilege. Treasury bills and money market funds were literally paying 0%. You could push into long-term Treasuries for a modestly higher 1.5% yield, but who really wants to take that kind of risk for so little yield? Junk bond ETFs paid around 4%, but, again, is the risk really worth it?

Flash forward to today and it's a much different environment. Now, investors really need to weigh the risk/return profile of both equities and fixed income to figure out which is better. With current yields on the short end of the curve at around 5%, there's a real debate. Do you invest in stocks and try to get a 10%+ return but face a very uncertain economic environment or do you take the 5% ultra low-risk return from cash and/or short-term bonds and call it a day?

The answer to that question, of course, is specific to the individual, but there's real appeal to choosing the latter. If you're really concerned about global recession and a market crash, why not just invest in a 1-year Treasury bill, lock in a 5.06% yield (as of 5/22/23) and regroup again in 2024?

ETFs aren't necessarily the same as buying a single T-bill and locking in a yield, but they can get you pretty close. Whether you want to stick to the safety of Treasury bills or are willing to take the next step and consider corporate bonds as well as government issues, there are some very good ETFs available that give you that exposure for your portfolio.

Let's take a look at a few of the best.

iShares 0-3 Month Treasury Bond ETF (SGOV)

Just recently, I wrote a piece comparing and contrasting SGOV with arguably the most popular T-bill ETF out there, the SPDR Bloomberg 1-3 Month T-Bill ETF (BIL). In that matchup, I went with SGOV due to its mostly similar risk profile but slightly higher yield, so it makes sense to choose it here as well.

As the name suggests, SGOV invests in Treasury bills with remaining maturities of three months or less, but overweights to the 0-1 month bucket. Its effective duration of just 0.1 years means that the fund has very little interest rate risk and its holdings are backed by the U.S. government. If you're investing in the fixed income ETF space, this is about as conservative as you can get.

Its current yield is 4.85% and comes with an expense ratio of 0.05%.

U.S. Treasury 3-Month Bill ETF (TBIL)

TBIL is a relative new entrant into the ultra-short income ETF space. It's a more unique product in that targets the most recently issued 3-month Treasury bill and only that bill. Once a new 3-month T-bill is issued, the fund rolls its holdings into that new bill. Whereas funds, such as SGOV typically holds maturities across a pre-determined range, TBIL targets a very specific single maturity.

TBIL is a real up-and-comer in this space and the ability to own a single Treasury maturity without needing to go through the U.S. Treasury directly clearly has appeal among investors. This fund has only slightly more risk that SGOV because its average maturity will be slightly longer, but investors could find the minimal extra risk worth it in order to capture the extra yield.

A 3-month Treasury bill currently yields 5.30%. TBIL comes with an expense ratio of 0.15%.

PIMCO Enhanced Short Maturity Active ETF (MINT)

MINT could be considered the next step up in risk, but it has a very different look compared to the two ETFs mentioned already. MINT is an actively-managed fund that invests primarily in global investment-grade corporate bonds with a remaining maturity of one year or less. Its effective duration of 0.25 years indicates that there's a bit more interest rate risk involved, but you're also introducing credit risk into the equation, something that mostly doesn't exist in Treasury bill funds.

Like many investment-grade bond funds, MINT dips into the lower rungs of the investment-grade credit ladder in order to maximize yield opportunities. To its credit, it has a much lower percentage of assets dedicated to the BBB-rated bucket than many of its peers. That makes it ideal for low risk income seekers who want to keep principal safety a priority, but want to squeeze a little more return potential out of their investment.

Its current yield is 5.26% and comes with an expense ratio of 0.36%.

JPMorgan Ultra-Short Income ETF (JPST)

JPST is a fund that is built similarly to MINT, but has a slightly different objective. Instead of targeting a specific maturity range, it targets a portfolio duration of 1 year or less. That means it carries more interest rate risk and potentially invest in longer maturity notes. Currently, it has about 80% of assets invested in notes with a maturity of one year or less and 20% in 1-3 year maturities. That makes JPST a bit more aggressive than the funds we've discussed so far, but still conservative enough that it falls into the low risk category. The current duration is 0.76 years, so it's coming in well below that 1 year ceiling.

JPST invests in a very diverse mix of short-term investment-grade corporate bonds, commercial paper, CDs and cash equivalents. The fund also has just 12% of its assets in the BBB category, so overall credit quality is higher than you'll find in other peer ETFs.

Its current yield is 4.83% and comes with an expense ratio of 0.18%.

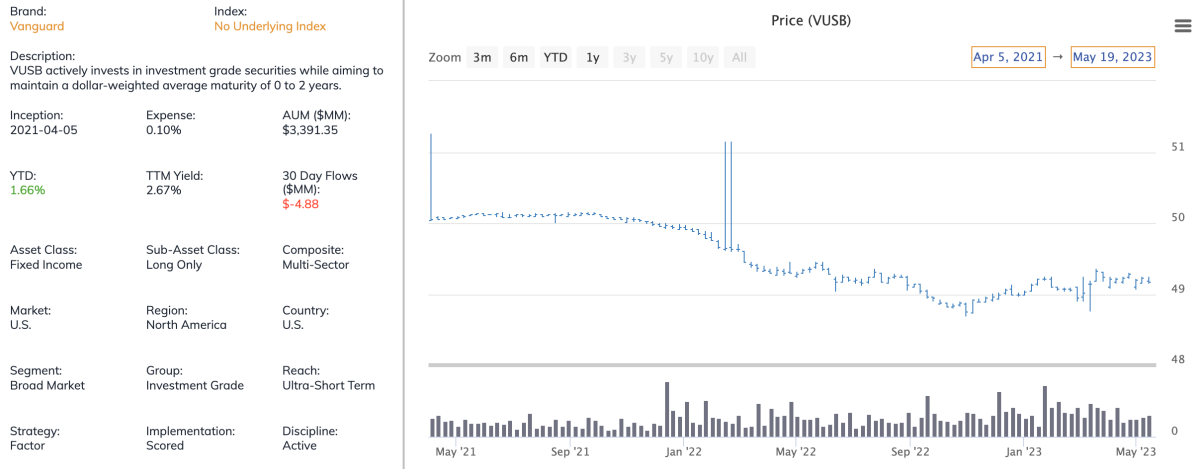

Vanguard Ultra-Short Bond ETF (VUSB)

VUSB would represent the furthest step out on the risk spectrum of all the ETFs on this list. It is also actively-managed targeting investment-grade corporate bonds with a goal of maintaining an average maturity of 0-2 years. It maintains a duration of 1 year, making it the most interest rate sensitive fixed income ETF of the bunch. While everything in the portfolio is rated investment-grade, it has worst credit profile with about 1/3 of the fund's assets in the lowest BBB-rated bucket.

If you're looking for a cash alternative, this is probably about as far out on the risk spectrum as you want to go. You can see by the chart above that share price fluctuation, historically, has been quite low, but it is potentially vulnerable to more significant moves in interest rates. This is the type of fund where active management can really help because it allows the portfolio to be according to the current environment.

Its current yield is 4.98% and comes with an expense ratio of 0.10%.

Originally published on TheStreet.com