Oversold stocks are what their name implies: stocks that have traded lower than they should, based on their fundamentals. It’s a subjective measure, of course; after all, for every seller, there’s a buyer. The key to success in buying into an oversold stock is recognizing when it’s getting near the bottom. These stocks typically make a comeback, even if they take their time about it. But once they do bounce, the potential for strong gains is very real.

We can check with Wall Street’s stock analysts to find which bargain-priced stocks are primed for gains. Once we know which stocks the experts recommend, we can start digging into their details. The data tools at TipRanks are ideal for this, letting us sort out stocks by a wide range of factors. The stock data plus the analyst commentary will together paint a comprehensive picture of any stock – a vital step before investing.

So let’s put that into practice. We’ve looked up the details on three stocks whose price is close to a one-year low – but which all have a Moderate or Strong Buy rating from the analyst community, and a one-year upside potential of at least 90%. Let’s take a closer look.

Criteo SA (CRTO)

We’ll start with Paris-based Criteo, an AI-powered online commerce and advertising media company. Criteo employs some 2,700 people, operates in 96 countries, and its commercial media ad display platform boasts over 685 million users per day along with 35 billion daily browsing and buying events. The company uses data analysis to drive effective commercial outcomes, and to enrich the consumer’s internet experience. Criteo operates on the popular pay-per-click (PPC)/cost-per-click (CPC) models.

Criteo has seen consistent strong revenues over the past few years. The top line in 2020 came in at $2.08 billion, and that improved to $2.25 billion in 2021. Last year, the first three quarters all showed year-over-year revenue gains.

Q4, however, showed a slight drop in revenue from the prior year. The 4Q21 top line came in at $653 million, down from $663 million in 4Q20. While revenues dropped slightly in that final quarter, adjusted EPS rose. Earnings were reported at 98 cents per share in 4Q20, growing to $1.44 per share in 4Q21.

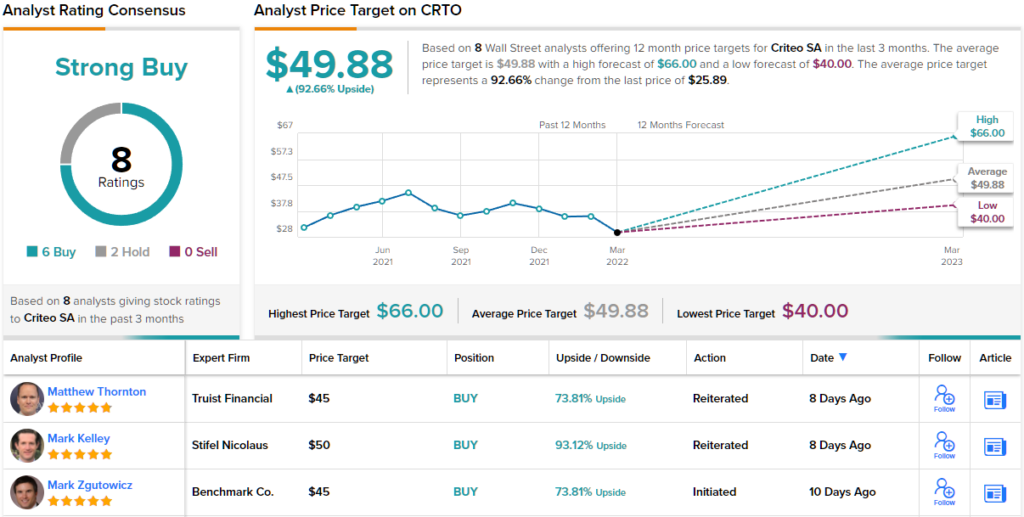

Investors should note that CRTO shares hit a peak value in December of last year, and since then have been falling. The stock is down 37% in the last three months.

Berenberg analyst Sarah Simon is unworried by the fall in share prices, and sees it as a chance for investors to move in on the stock.

“While Criteo is set to deliver double-digit growth in 2022, with an accelerating run-rate as the year progresses, the stock is valued as if it is going out of business. We continue to believe that Criteo is well positioned to weather the deprecation of third-party identifiers, including that which was announced by Google last week, given its evolving business mix and extensive first-party integrations. Valuation completely fails to reflect this, in our view,” Simon opined.

These comments support Simon’s Buy rating, while her $66 price target indicate potential for a strong 153% upside in the year ahead.

The Strong Buy consensus rating, based on a 6 to 2 split between Buys and Holds, shows that Wall Street, too, is bullish here. The stock is selling for $25.89 and its $49.88 average price target suggests it has a one-year upside of ~91%.

RingCentral, Inc. (RNG)

Let’s shift gears, and take a look at a tech company. RingCentral is an SaaS firm, bringing telecom to the desktop computer and the office network server, offering a range of business communications solutions – phone lines, extensions, call forwarding, video calling, screen sharing – making them compatible with popular applications like Outlook, Salesforce, and Google Docs, and giving customers the whole package on the cloud. It’s business telecom is also available on an app.

RingCentral has seen 8 consecutive quarters of top-line revenue growth, with last quarter, 4Q21, coming in at $448 million for a 34% year-over-year gain. Quarterly earnings were also strong – at 39 cents per diluted share, EPS beat the 37-cent forecast and grew 34% from 4Q20.

Full year results from 2021 were also solid. Revenue was up 35% y/y, to $1.6 billion. That total was driven by a 36% gain in subscription revenue, which hit $1.5 billion in the year. Adjusted EPS for the year was $1.34, up from 98 cents in the prior year.

Now look back at the description of RingCentral’s product and service, and the reason for the surge in sales and earnings is clear. This company was superbly suited to thrive during the work-from-home push in the corona crisis. However, the prospect of a ‘return to normal’ has investors worried that RingCentral will see a decline in sales as office locations reopen. For the past year, the stock is down ~70%.

5-star analyst Terry Tillman, of Truist, believes that the price decline in RNG is a buying opportunity, and he is not shy to say so.

“The company has remained a model of execution, beating numbers and raising its outlook on an ongoing basis. The company has proven to be a sustained 30%-plus grower for well over a decade, and we certainly expect the upside case in 2022 to reflect similar growth/momentum… Currently, the shares trade at a meaningful discount to 30%-plus growers… We recommend investors buy the shares owing to increased confidence in sustained strong top-line growth while showing profit and cash flow progression,” Tillman wrote.

In line with this upbeat outlook, Tillman rates RingCentral’s shares a Buy, describing it as ‘strong by almost any measure.’ His $295 price target suggests an upside of ~181% in the next 12 months.

Overall, RingCentral has a stellar reputation in the tech world, and has attracted no fewer than 23 ratings from Wall Street’s analysts. These include 20 Buys against 3 Holds, for a Strong Buy consensus view. RNG has an average price target of $235.48, implying ~125% upside from the $104.95 trading price.

NeoGames (NGMS)

For the last stock on our list, we’ll stick with the tech sector – but look at an aspect of it as different from RingCentral as a company can get. NeoGames, with 15 years’ experience, is a tech provider for the iLottery niche, making gaming solutions available for national- and state-regulated lotteries. These games have long been popular, and that popularity has readily transferred to the online world. NeoGames has capitalized on that fact – and has accumulated over 42 million player accounts.

To raise capital, the company went public in November of 2020. It announced initial pricing of the offering at $17 per share, to sell just over 4.8 million shares; in the event, NeoGames sold over 5.5 million shares, and raised $94 million.

Since the IPO, however, NeoGames has seen revenues and earnings decline, along with share price. From the fourth quarter of 2020 to the fourth quarter of 2021, the top line fell from $14 million to $12 million. Worse, the company posted a ‘comprehensive loss’ in 4Q21 of 14 cents per share, comparing unfavorably to the 10-cent EPS profit of the year-ago quarter, and far below the 9-cent profit expected. The stock peaked in value above $70 per share in June of 2021, and is currently down 80% from that level.

Stifel’s Steven Wieczynski, rated 5-stars by TipRanks, believes that this stock is a true bargain for investors, and that the perceived risk is worth it when compared to upcoming gain potential.

“NGMS shares have come in considerably since their mid-2021 highs, driven by a combination of factors including 1) fading stay-at-home demand tailwinds, 2) limited new state catalysts, 3) decelerating margins, as well as more recently 4) potentially rising interest rates, and 5) geopolitical driven risk-off market. We believe sentiment on stock-specific headwinds has likely bottomed out, with extremely conservative current valuation affording investors an opportunity to play a multi-year secular growth story with 1) considerable barriers to entry, 2) stable, predictable, and robust margins and FCF conversion, and 3) still forthcoming new state catalysts,” Wieczynski explained.

To this end, Wieczynski gives NeoGames a Buy rating with a $34 price target that indicates room for ~144% upside by the end of 2022.

While there are only 3 reviews of this stock on record, they all agree on the bullish side, making the Strong Buy consensus rating unanimous. NeoGames is trading for $13.96 and its $36.67 average price target suggest it has a 163% one-year upside potential.

Originally published on TipRanks.com

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.